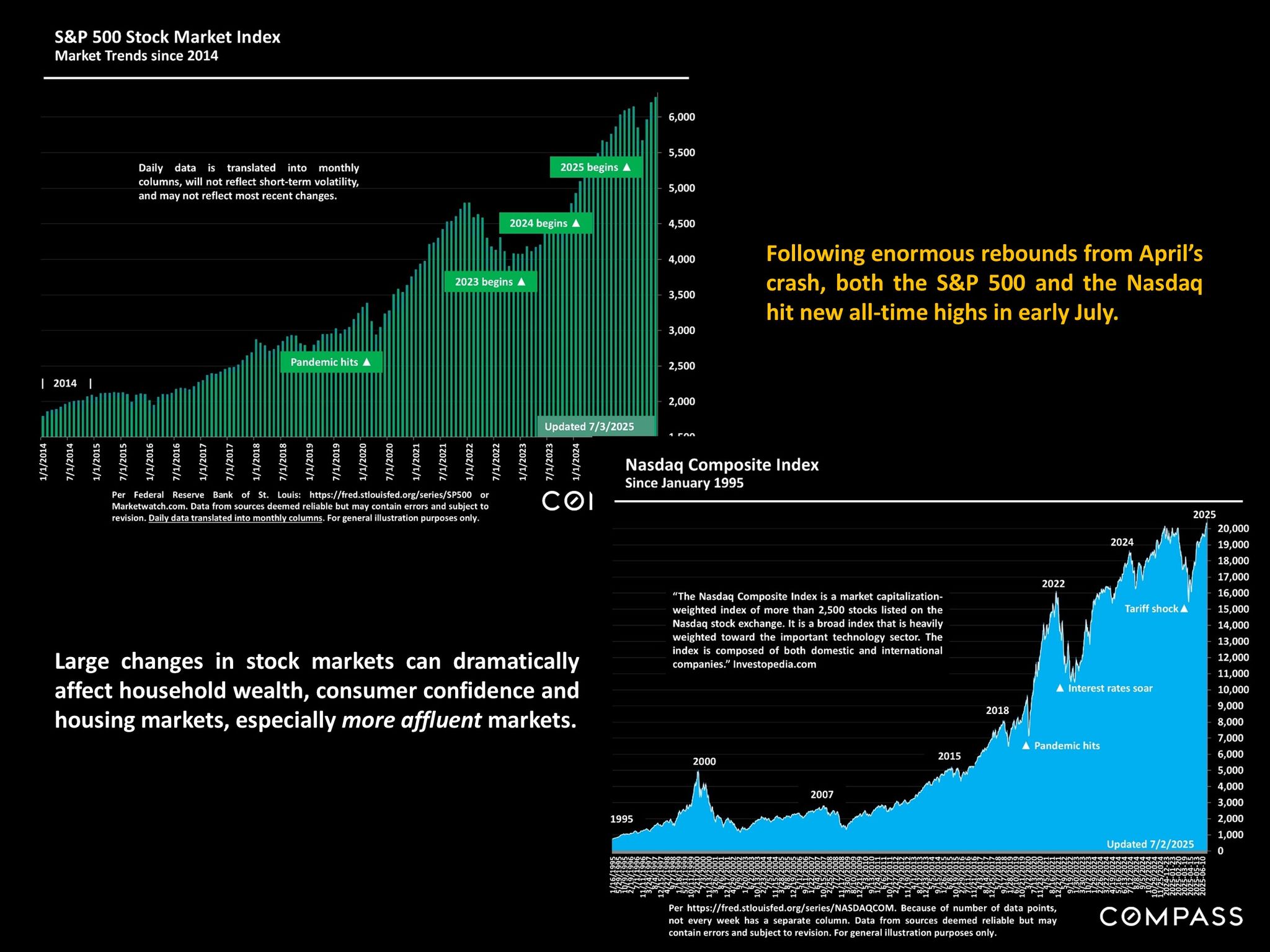

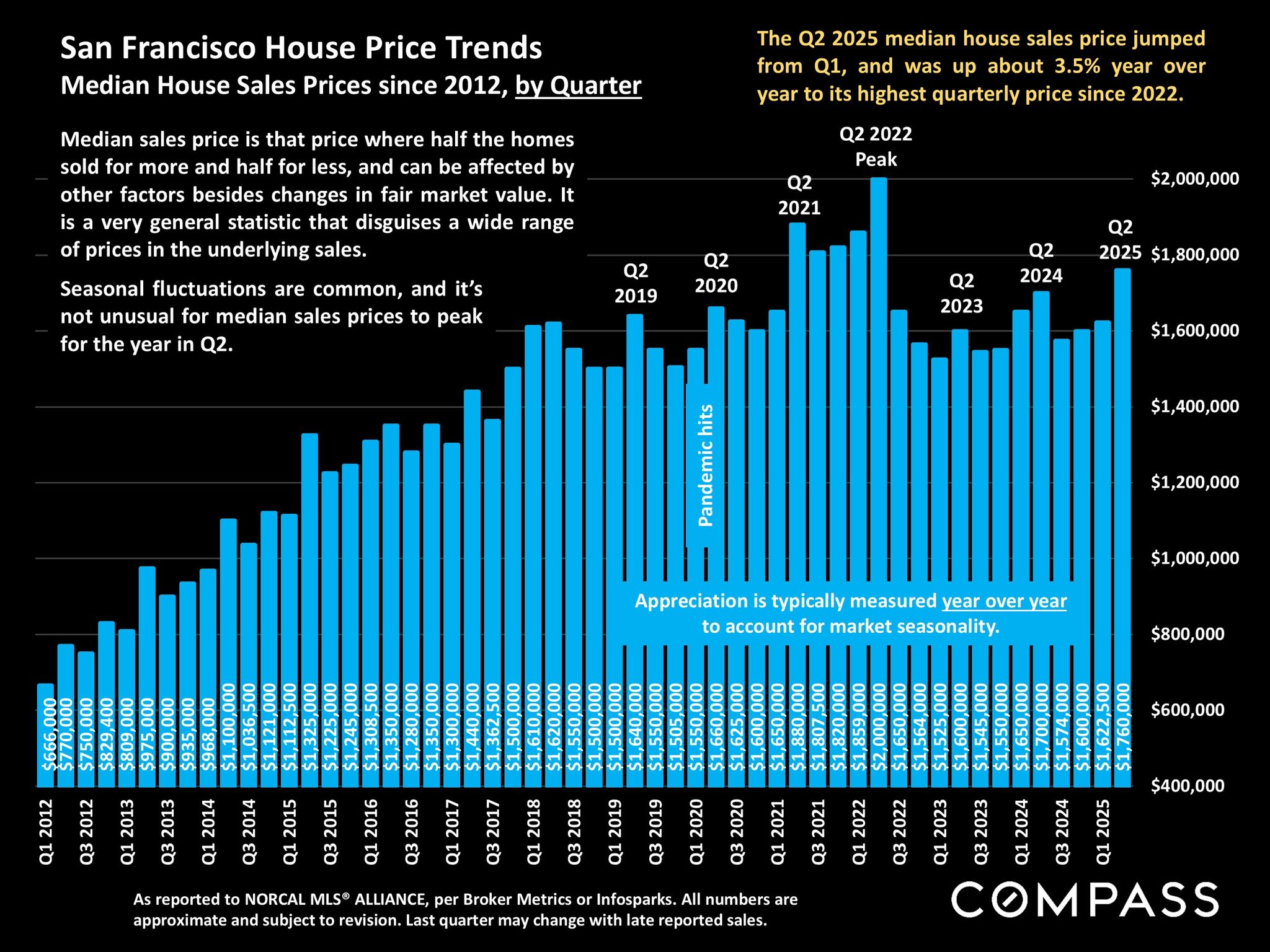

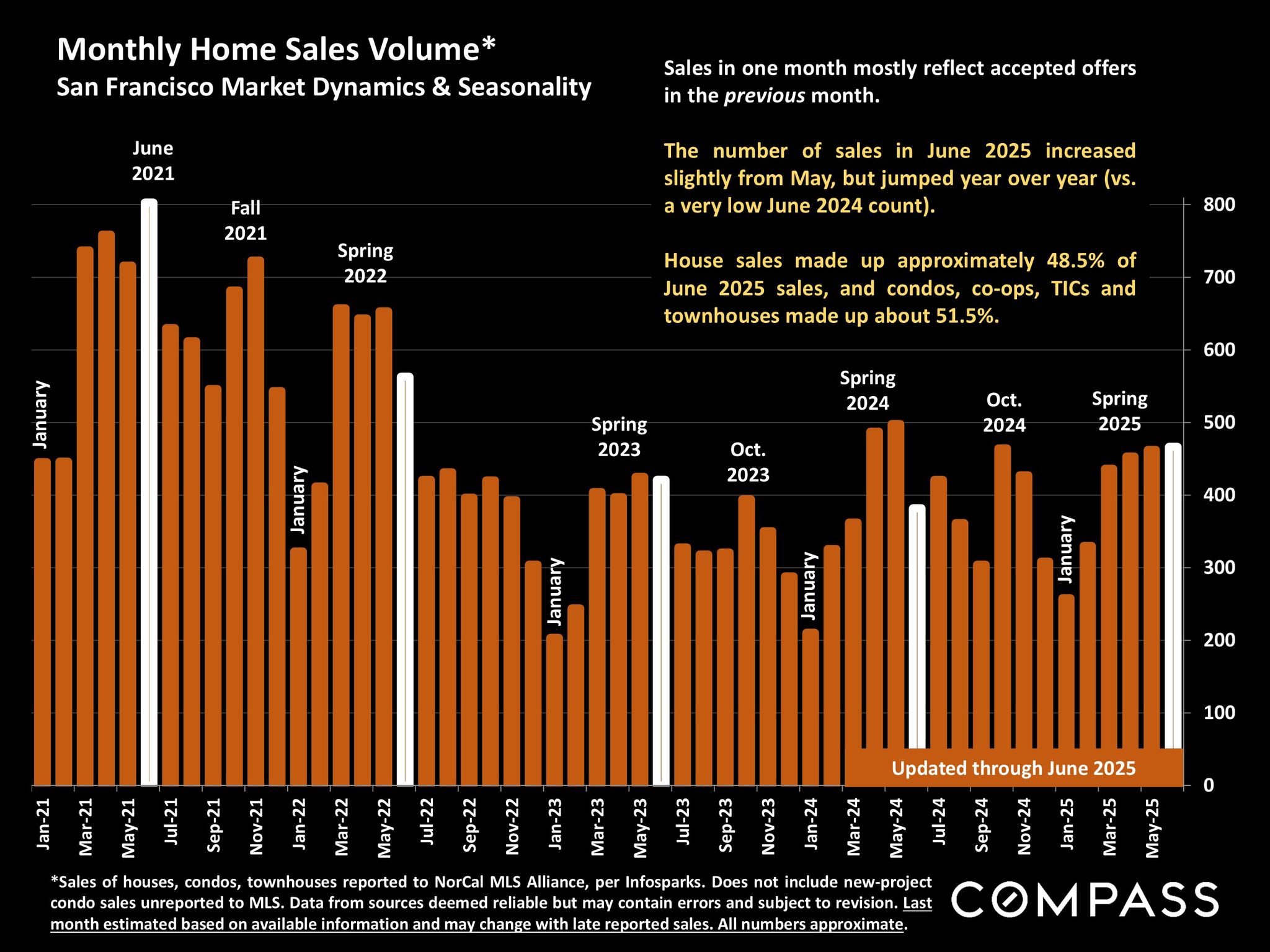

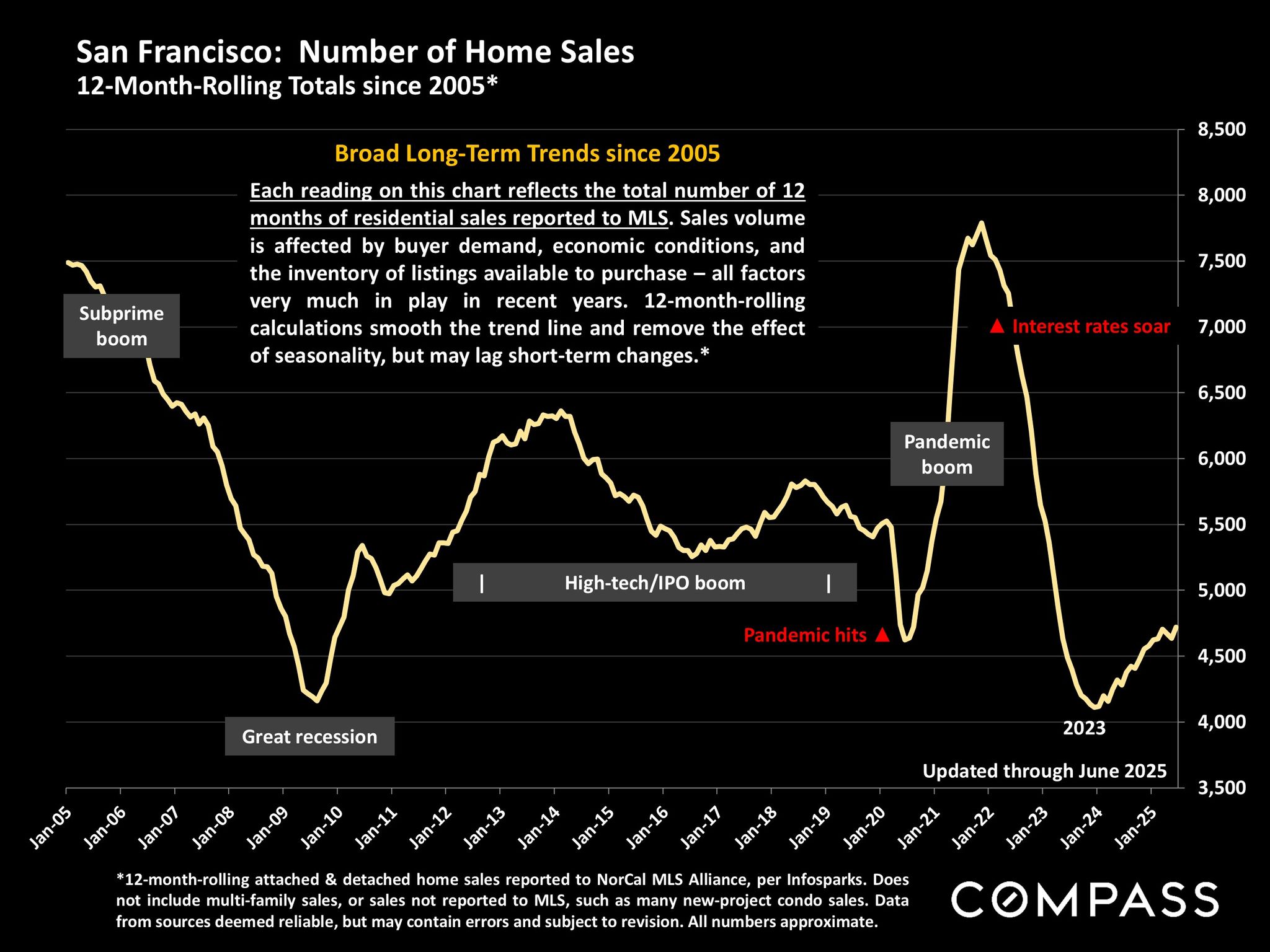

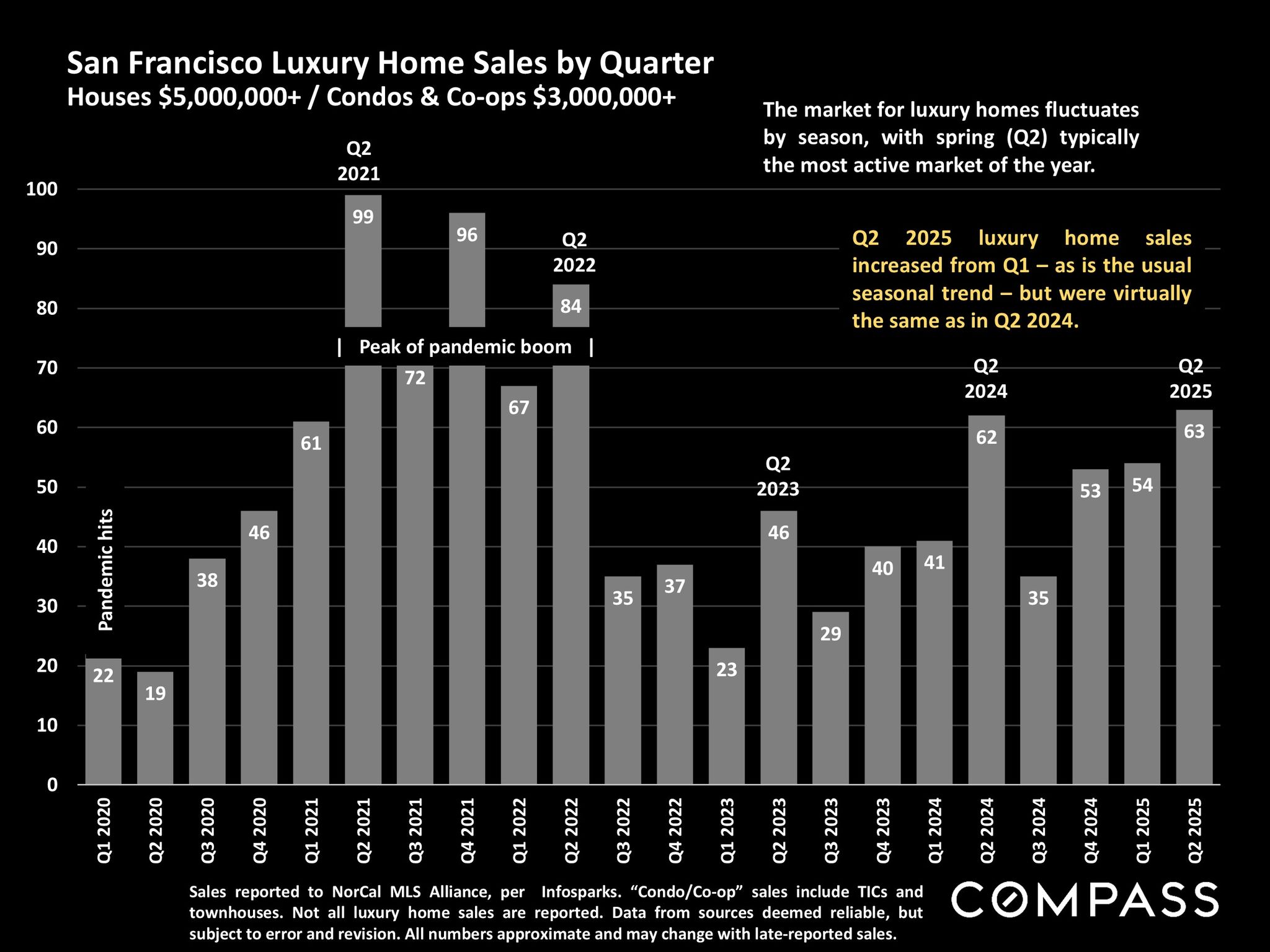

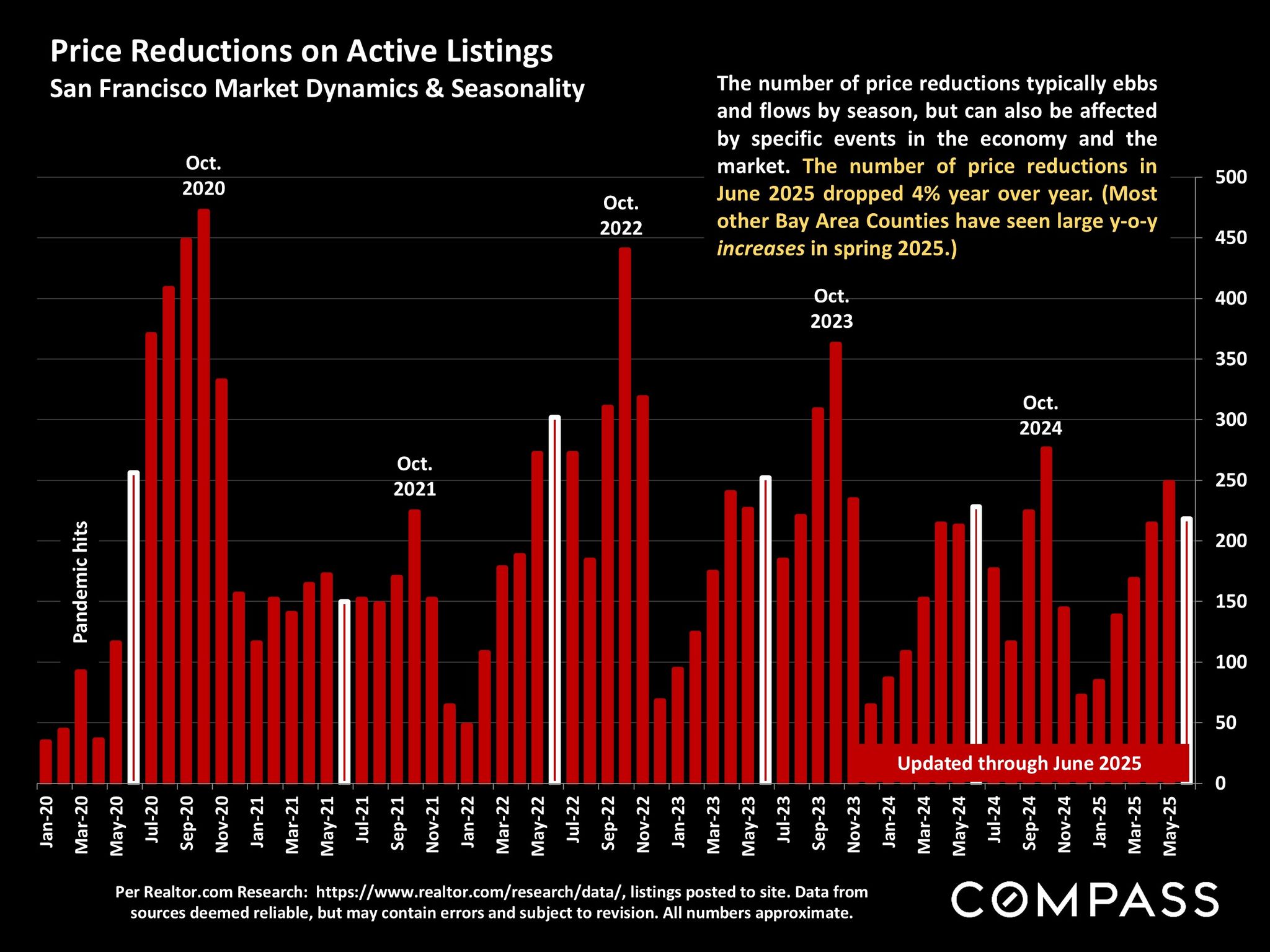

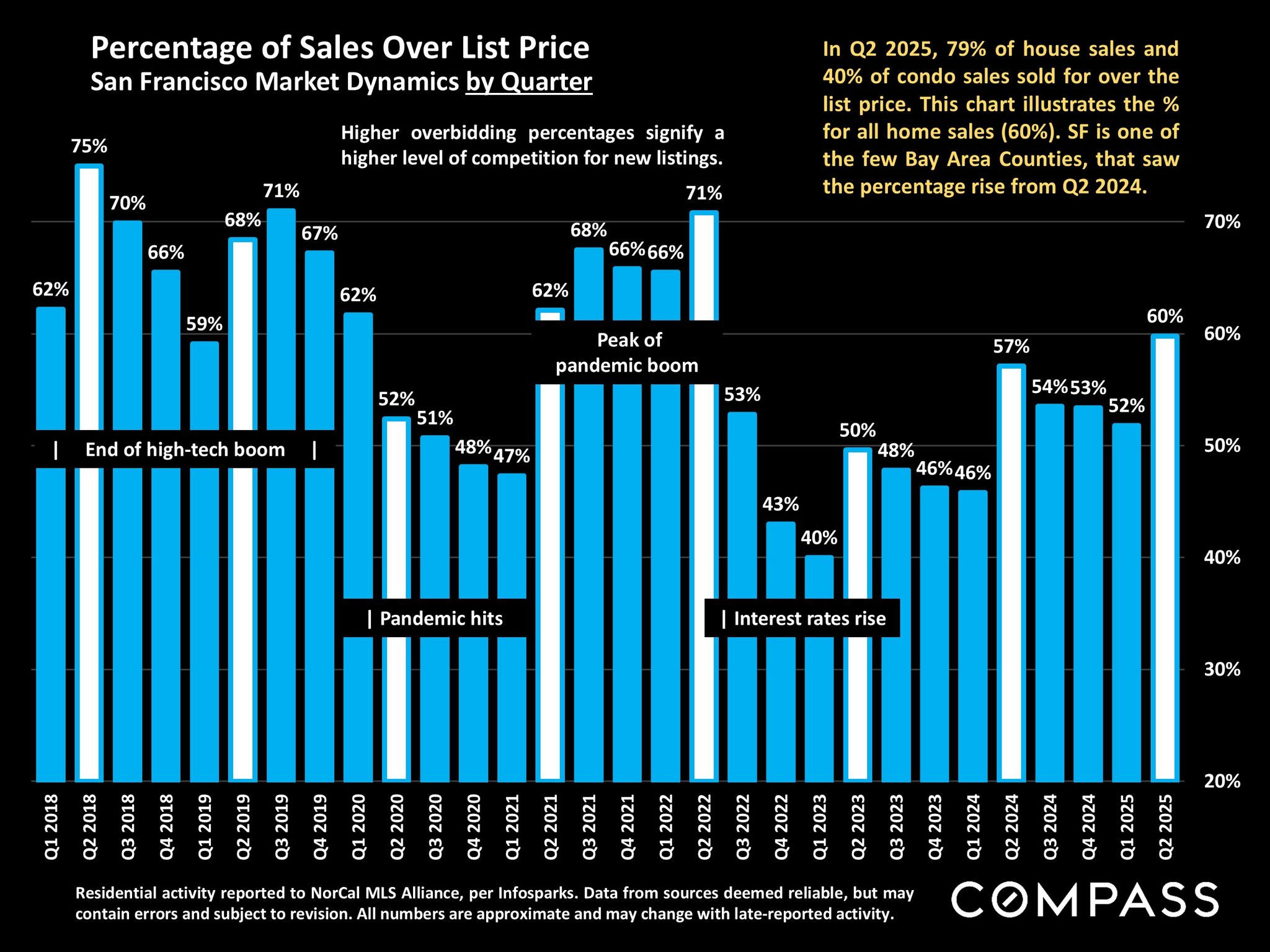

Across most of the Bay Area, the severe economic volatility which prevailed in Q2 – and the absence of a meaningful decline in mortgage interest rates – generally caused a significant year-over-year weakening in the spring selling season, usually the most dynamic of the year. However, this did not occur in San Francisco, whose indicators of supply and demand – illustrated in this report – either strengthened or remained essentially unchanged from Q2 2024. The median sales prices for both houses and condos hit their highest quarterly points since the peak of the pandemic boom, and apartment rents were the highest since 2020. Though one has to assume the market would have been even stronger if the macroeconomic conditions had been more favorable, the SF market remained quite robust. Furthermore, as of early July, measures of economic uncertainty were dropping, stock markets had staged an astounding recovery to hit new highs, consumer confidence had begun to rebound, and interest rates were gradually declining. Improvements in these conditions, should they continue, may support an even more heated market in the second half of the year. As always, correct pricing, preparation and marketing are imperatives for sellers desiring the best results. And opportunities exist for buyers who keep a close eye on both new and older listings, monitor time-on-market and price reductions on unsold homes that meet their requirements – or perhaps need a little bit of work – and are prepared to move quickly and aggressively.

Check out this article next